Evening Wrap: ASX 200 higher on surging resources sector, gold, copper, and lithium stocks lead way

Thu 04 Jul 24, 5:36pm (AEST)

Over the last few days three separate dedicated reports on lithium have dropped on my desk from three of the biggest research teams in the business: Morgan Stanley, Citi, and UBS. Each broker’s research team closely follows the lithium story, and I have reported their respective views here many times in the past.

The brokers’ research teams leverage their vast resources to monitor developments in the lithium market in major producer and consumer China, as well as across the globe. It’s therefore prudent to keep tabs on their latest views, of which I provide a summary for you today.

The broker’s analysts just attended the Fastmarkets Lithium Conference in Las Vegas last week. Their key takeaways from the conference are as follows:

The risk-reward for lithium is improving, “but we are not there yet”.

The broker cites the demand slowdown for EVs as a key demand-side factor, noting “EVs need to close down the ~15% price premium [to ICE’s] to balance range and residual value concerns”.

The broker cites the recent “supply jump” and thus far “lack of material project closure” as key supply-side factors.

The broker believes the lithium market continues to require a “rebalance” and this can only be achieved if prices fall to US$8,000-US$10,000/t, after which may “drive a new cycle”.

The broker notes “Many spodumene players are not profitable at current prices, but we believe we may not see material closures if LCE prices do not fall to the 8-10k range”.

The broker notes “The faster and further prices fall … the faster supply should leave the market”.

The broker is still waiting for a final “supply capitulation” before they’re ready to call the bottom.

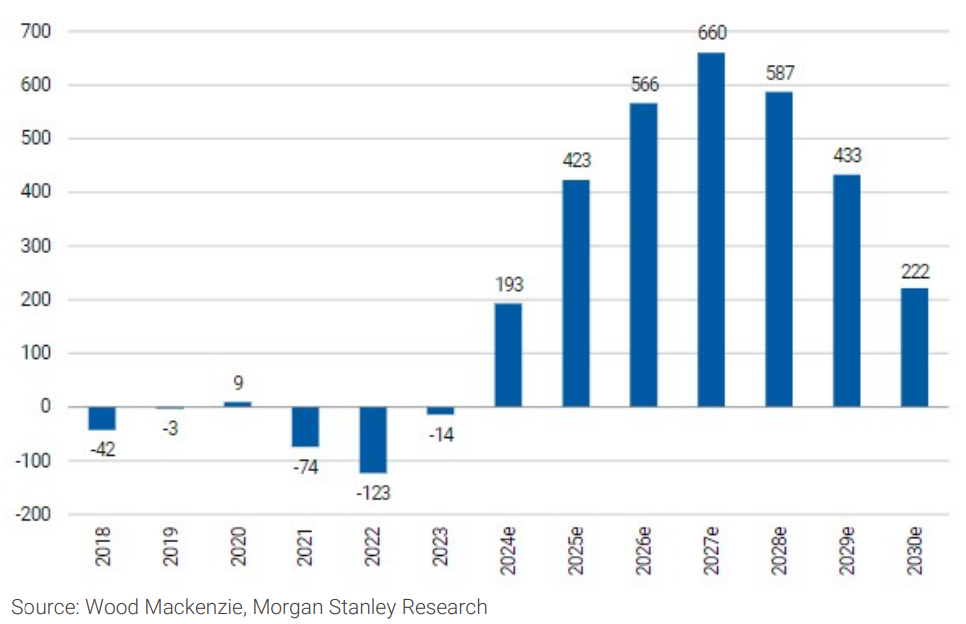

The above Exhibit from Morgan Stanley shows lithium carbonate equivalent (LCE) deficits/surpluses since 2018, and the broker’s forecasts until 2030. Note that large deficits in 2021 and 2022 corresponded with an exponential increase in lithium prices in those years. The rebalance since 2023, as new supply came on stream, has triggered a similarly sharp price decline.

Also interesting is this Exhibit from Morgan Stanley that shows the production cost curve for lithium producers. The average cost of production in LCE terms is US$12,263/t. As stated above, Morgan Stanley believes that the lithium carbonate price must fall to US$8,000-US$10,000/t to knock out enough production to rebalance the market (note, the current price is US$12,500/t).

Citi is well known for its bearish short term views on lithium, as I have reported, taking out short positions in lithium futures contracts since April. Here are the key takeaways from their latest report:

“Visible inventories are rising, with the latest datapoint suggesting inventories have increased by ~70kt (annualised basis) since the start of the year”.

“This high and rising low-shelf-life chemical inventories should see lithium prices fall another 15-20% to $10k/t”.

“Prices around these levels are expected to eventually lead to mine/converter closures and industry rationalisation, alleviating our modelled extremely large surpluses”.

The above Figure from Citi is similar to the last Exhibit from Morgan Stanley. It shows the current price of lithium carbonate remains above many producers’ cost bases. Note that if Citi’s target of US$10,000/t is correct, it would likely knock out at least some supply from Chinese lepidolite producers.

UBS has been relatively quiet on lithium for some time, so for me, it makes Friday’s note even more interesting within the context of the recent plunge in lithium prices. Here are the key takeaways from their latest report:

“Despite the weak demand outlook, we continue to see new supply come to the market…lithium markets remain well-to-over supplied”.

“We expect prices to stay lower for longer and have extended market surpluses in our forecasts”.

Broker cites “weak ex-China demand on stagnating penetration rates, rising PHEV share, and the rollback of EV targets/support and increased protectionism by western nations” as a key demand-side factor.

On the supply-side, the broker notes “we continue to see new growth and have added significant new supply in this update”.

“We have lowered our lithium price forecasts with spodumene SC6.0 CFR China -10%/-7%/-4%/-10% over 2024/25/26/27E to US $1,015/1,000/1,100/1,300t.” (The broker notes they now sit around 20% below consensus forecasts).

As for ASX lithium stocks, UBS states: “With increased uncertainty on the long-term demand outlook ex-China and continued opaqueness on near-term supply additions from China/Africa, we remain underweight the sector”.

The broker retained their SELL ratings on: Pilbara Minerals (ASX: PLS) with the stock’s price target lowered to $2.50 from $2.70; on Mineral Resources (ASX: MIN) with the stock’s price target lowered to $56 from $58; and on IGO (ASX: IGO) with the stock’s price target lowered to $5.95 from $7.35.

Get the latest news and insights direct to your inbox